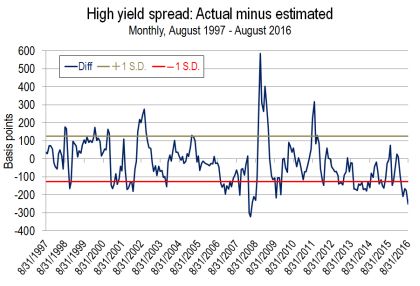

Marty Fridson, of Standard & Poor’s Global Market Intelligence, reports today that on September 8 the difference between the yield on junk bonds and the company’s estimation of fair value stretched to two-standard deviations of its long-term average. To understand just what this means, Fridson writes, “a divergence of just one standard deviation qualifies as extreme overvaluation in our analysis.” Two-standard deviations is far more rare than even this measure of “extreme overvaluation.” In fact, it’s the mathematical threshold Jeremy Grantham uses to define a financial “bubble.”

Chart via highyieldbond.com

Chart via highyieldbond.com

For what it’s worth, the last time junk bonds crossed this valuation threshold was May of 2008. They lost nearly half their value over the next ten months.