A version of this post first appeared in The Felder Report PREMIUM.

About a month ago former Fed head, Richard Fisher, came out and confirmed the idea that the FOMC’s quantitative easing policies over the past seven years have pushed prices of risk assets, including stocks, beyond what would otherwise be supported by their fundamentals.

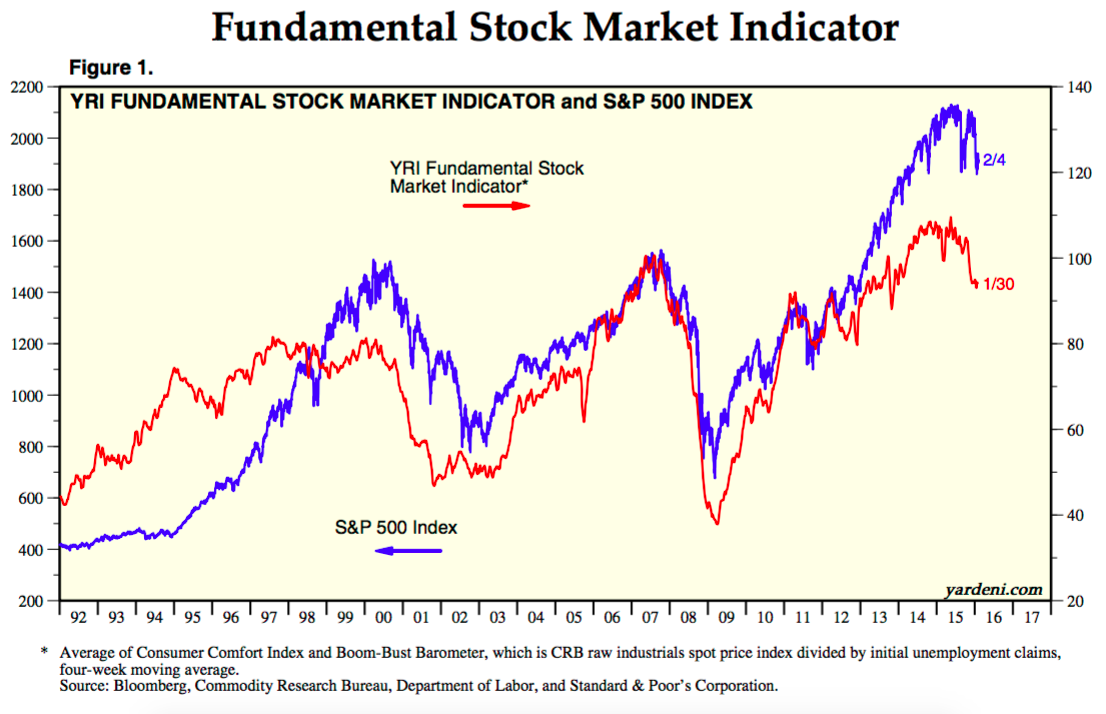

There are a few ways to visualize this. The first comes from Dr. Ed Yardeni who tracks a fundamental indicator shown below. Notice the yawning gap between the S&P 500 Index and the major economic fundamentals.

We can also just look at the index versus its components’ earnings. Here’s another gap:

This chart is a gift to anyone with common sense. Have a nice day.

S&P EBITDA vs Price pic.twitter.com/THCADhUwso— JP Compson (@JPCompson) February 4, 2016

And if you prefer to look at forward earnings estimates, you’ll find another massive gap:

Consensus Long-Term EPS Growth Rate Cut by 4th Largest Amount in 30+ Years I've Been Calculating It pic.twitter.com/zo0ZO22Boi

— Not Jim Cramer (@Not_Jim_Cramer) February 1, 2016

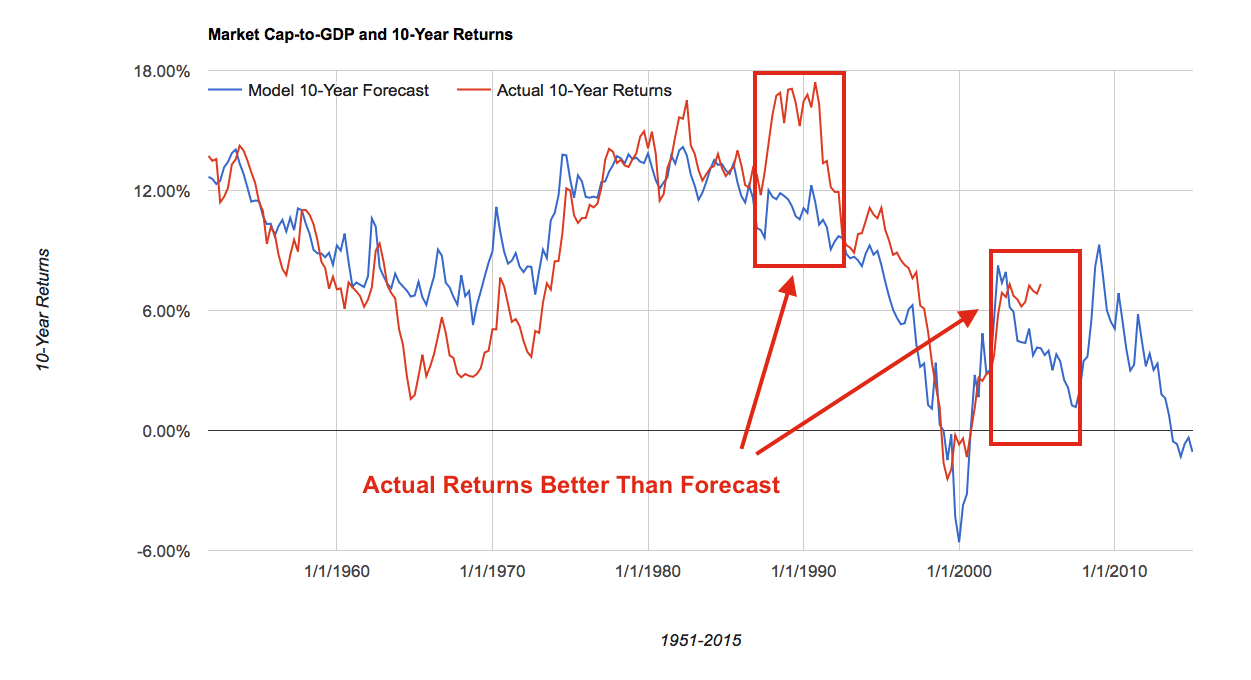

Specifically, Fisher said that the Fed had, “front-loaded a tremendous rally.” All this means is that the Fed pulled returns forward from the future to generate larger gains today. Notice in the chart below that returns have recently been significantly better than valuations (using the Buffett indicator) 10 years ago justified. This is exactly what Fisher is referring to.

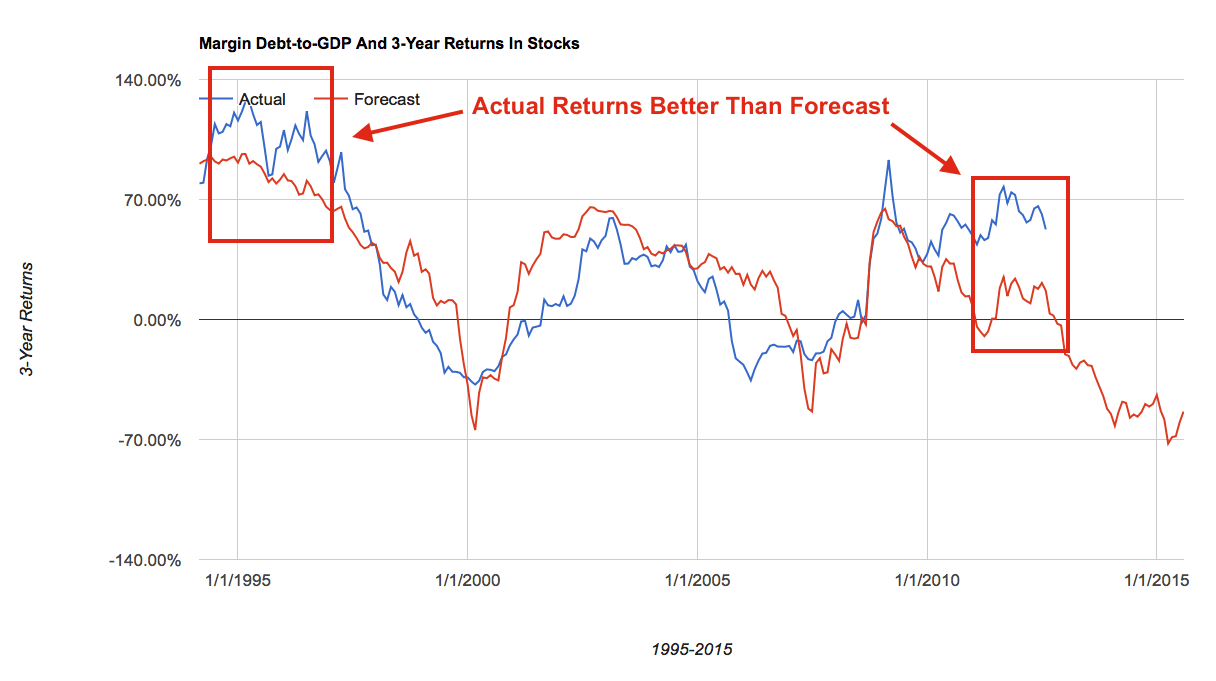

The last time this happened was in the late 1990’s. From that peak, stocks fell more quickly than forecast in order to play, “catch up,” to the downside. Interestingly, the 3-year forecasts I generate using margin data show the very same gaps in the late 1990’s and today.

And there are other indicators suggesting these gaps could close sooner rather than later. Bond market risk appetites (very similar to spreads in corporate bonds, junk bonds and leveraged loans) have been falling farther and for a longer period of time than stocks. These are normally very highly correlated to stock prices yet here is another major gap.

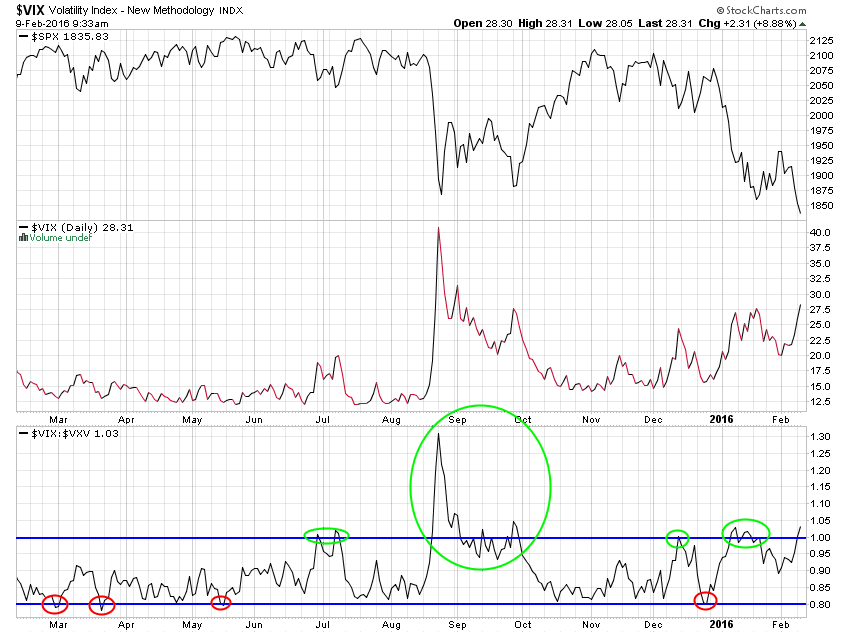

Another way to visualize this is to compare bond market risk appetites to stock market volatility. While fear in the bond market has soared recently, fear in stocks is relatively subdued. Notice the gap between them in the chart below.

So when Richard Fisher says he, “can see significant downside,” in the stock market right now, he’s probably thinking about these sort of gaps between stocks prices and economic fundamentals. Between stocks and their earnings. Between stocks and the corporate credit markets. Because he helped create them. And, like Dr. Frankenstein and his monster, nobody knows better what they’re capable of.