“Profit margins are probably the most mean-reverting series in finance.” -Jeremy Grantham

Just over a year ago I wrote a brief post simply pointing out how peaks in profit margins over the past couple of decades have preceded major peaks in the stock market. At the time, it looked as if record profit margins might be in the early stages of peaking, potentially flashing a warning for stocks. Since then, it looks as if the stock market may have followed in profit margins’ footsteps. The chart below plots the overall level of profit margins (blue line) alongside the year-over-year change in stock prices (red line):

Chart via FRED

Chart via FRED

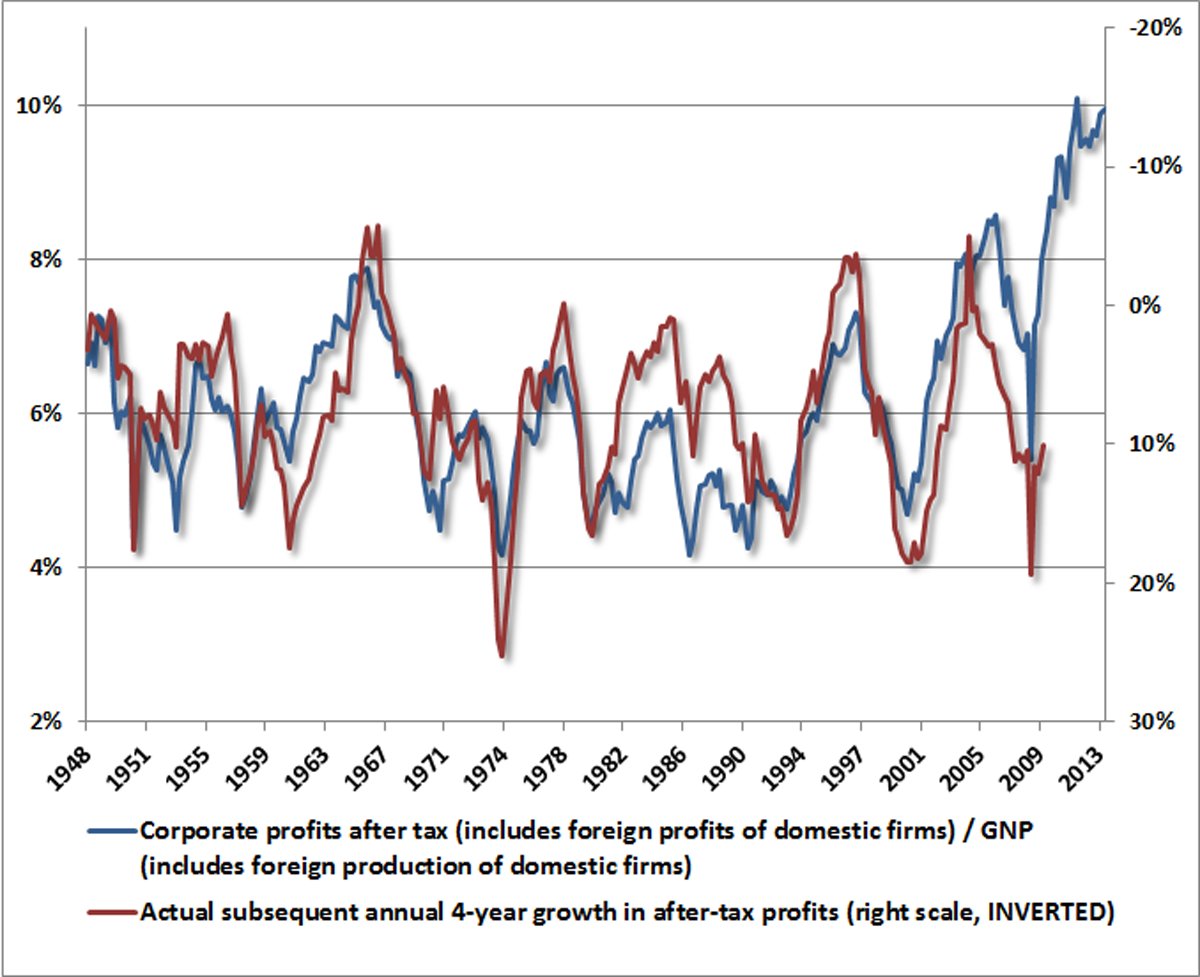

The reason I believe stocks and profit margins are so closely tied together is that profit margins are very good at predicting future earnings growth. As John Hussman recently demonstrated, high profit margins make for very low or negative forward earnings growth and vice versa:

Chart via Hussman Funds

Chart via Hussman Funds

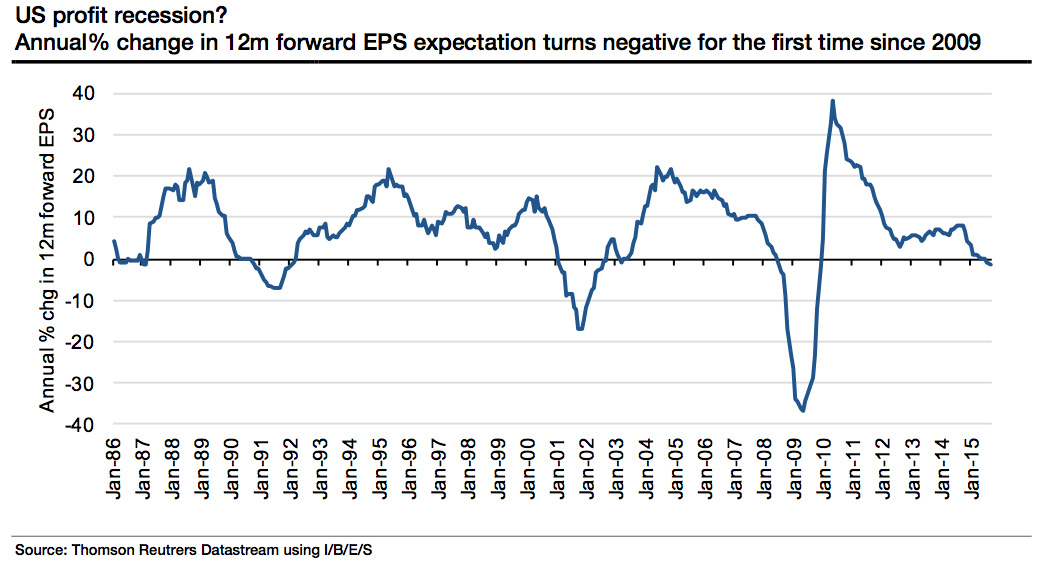

Having recently witnessed record-high profit margins, we should probably now be ready for a major decline in earnings growth. In fact, we might now be seeing only the beginning of this trend:

Chart via Business Insider

Chart via Business Insider

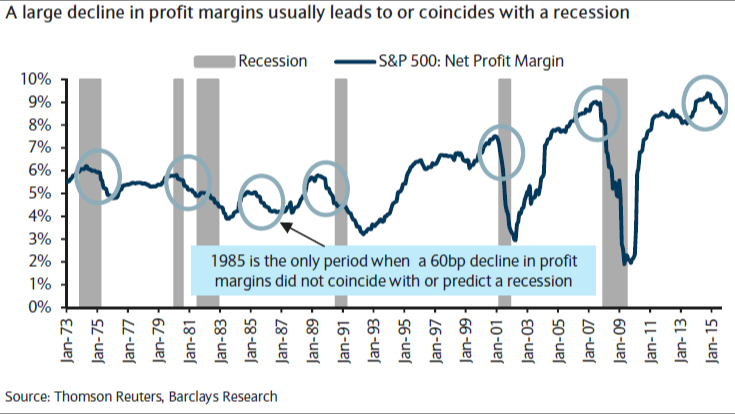

And if profit margins reverting to their long-term mean leads to falling earnings growth, is it any wonder that major peaks in profit margins don’t just foreshadow major stock market peaks but economic peaks, as well? The chart below comes from Barclays. It demonstrates that only in 1985 did the economy avoid entering recession after a 60 basis point decline in profit margins, the degree of decline we have just witnessed.

Chart via Business Insider

Chart via Business Insider

Clearly, record-high profit margins have been a significant driver of both the economy and the stock market over the past few years. But this, “most mean-reverting series in finance,” looks to be rolling over and now this powerful tailwind could is shifting into a headwind.