Stocks are just starting to notice what junk bonds have known for months http://t.co/RUugEkg3rA pic.twitter.com/QGRrQ4yOwn

— Jesse Felder (@jessefelder) January 5, 2015

The stock market has now given back almost all of its late-December gains and it looks like it’s finally starting to pay attention to the canary in the coal mine that is the junk bond market.

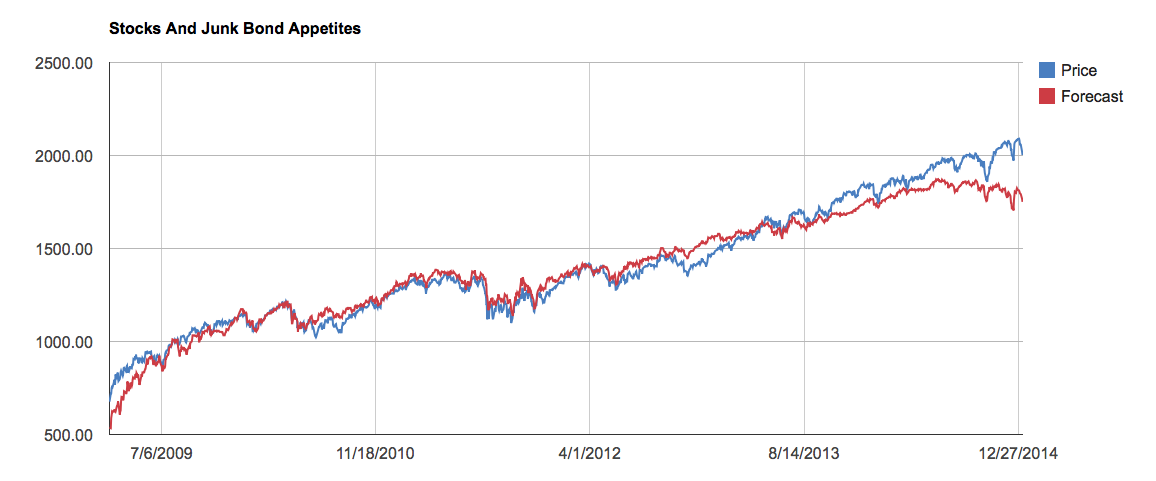

As I pointed out about a month ago, the divergence between stocks and junk bond spreads (see the chart in the tweet above) is critical because we saw similar action at the peaks in 2000 and 2007. In fact, today’s divergence is wider than either of those two precedents.

What’s remarkable about this to me is that over the past 7 years, junk bond risk appetites (as measured by the ratio between the high-yield ETF and the 5-year treasury bond) and stock prices have had a 98% correlation coefficient. So the recent weakness in junk appetites currently implies a price target of 1750 on the S&P 500 (based on the statistical forecast), or 12.5% lower than the current level.

This, however, is a moving target. A couple of weeks ago I wrote that this target stood at 1800. Because junk appetites have fallen since then, their implied target for stocks has, as well. Should junk appetites improve this target would move back up.

{kind=link}

But it’s important to note that if risk appetites are broadly shifting to greater risk aversion, as Howard Marks recently suggested they might be, this divergence could very well mean exactly what it meant back in 2000 and 2007.