The new Z.1 report came out today so let’s update many of the indicators I’ve been sharing here over the past few months. What should be worrisome to market watchers here is that we now have a host of significant indicators that look like they may have formed important peaks and begun to roll over. We will need to see at least a couple more quarters worth of data to be sure but this is certainly something to keep an eye on.

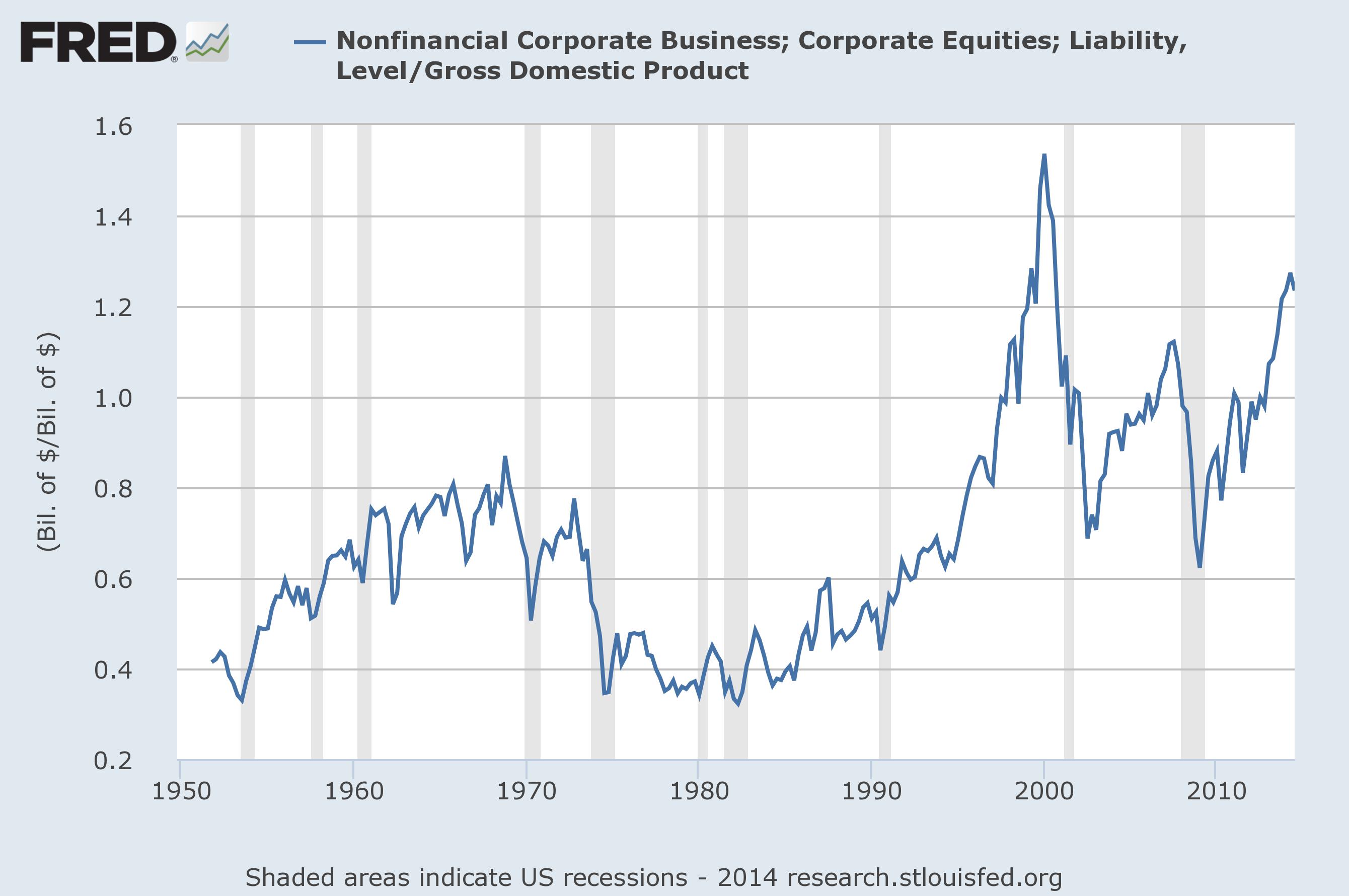

First let’s take a peek at Warren Buffett’s favorite valuation yardstick. (See “How To Time The Market Like Warren Buffett” for a look at one way I use this indicator.) It actually peaked last quarter and saw a small retracement in Q3. This indicator is 83% negatively correlated with future 10-year returns in stocks (the higher the reading the lower forward returns) and its current reading implies a -0.88% annual rate of return over the coming decade. The 10-year treasury at 2.2% looks fairly attractive in comparison.

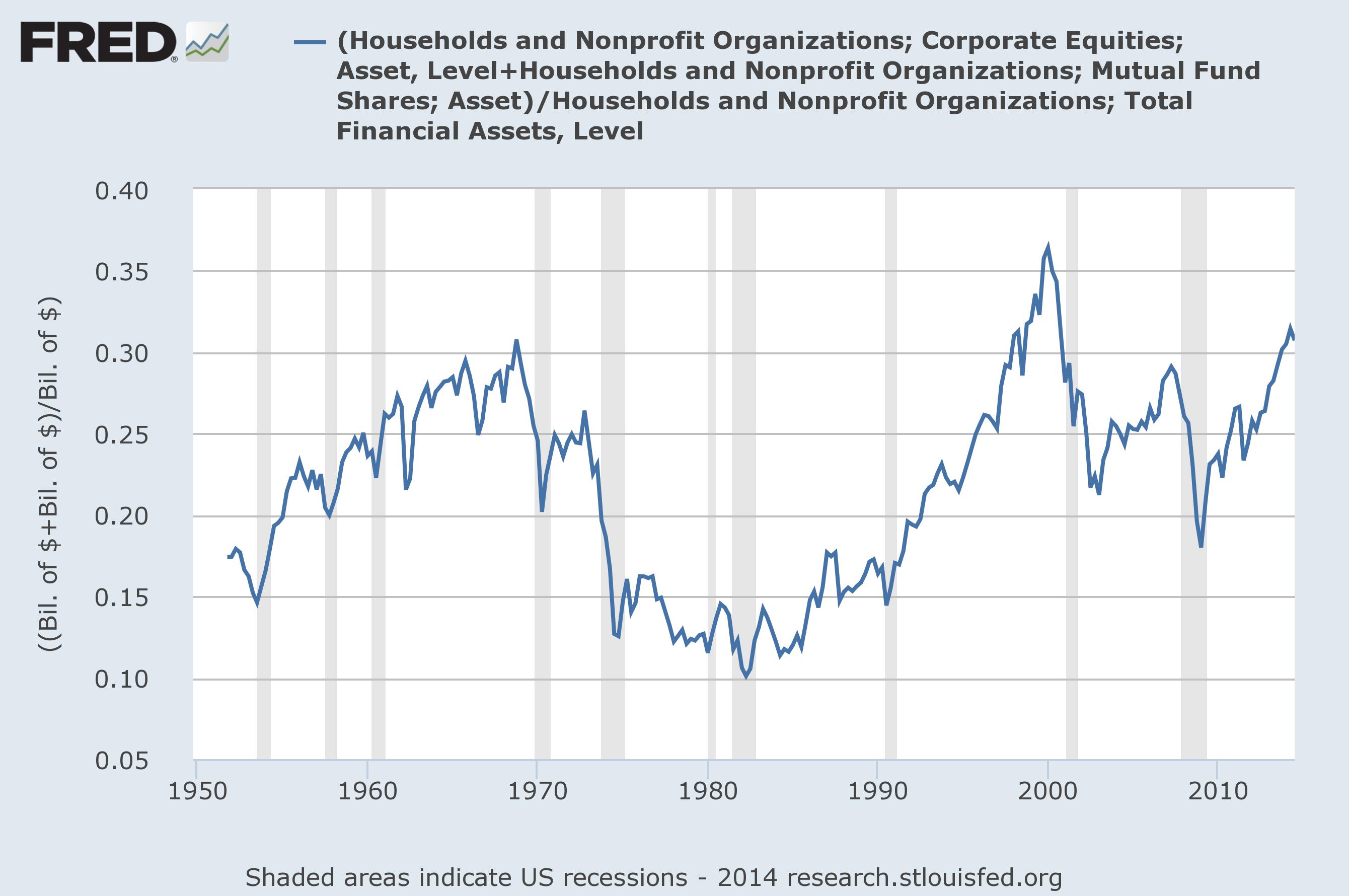

Next we can take a look at the household percentage of financial assets allocated to equities. This indicator is even more negatively correlated to future 10-year returns at about 90%. It has also pulled back just a bit from the peak it made in Q2. Its current reading implies a forward return of about 2.8% per year over the coming decade, slightly better than the 10-year treasury.

Next we can take a look at the household percentage of financial assets allocated to equities. This indicator is even more negatively correlated to future 10-year returns at about 90%. It has also pulled back just a bit from the peak it made in Q2. Its current reading implies a forward return of about 2.8% per year over the coming decade, slightly better than the 10-year treasury.

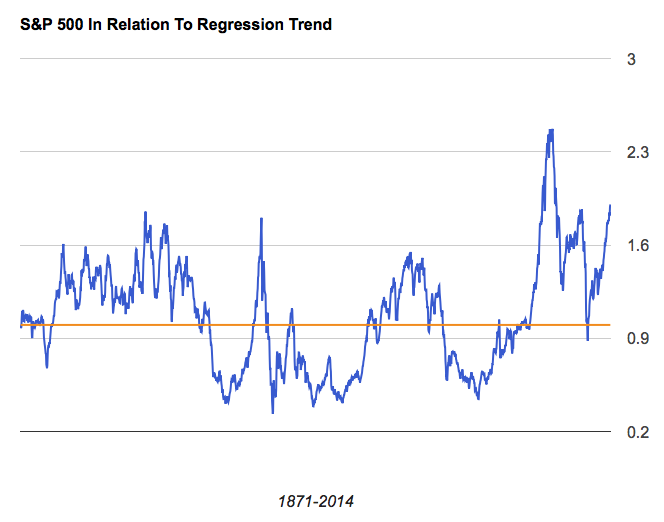

Finally, comparing the current level of the S&P 500 to its long-term regression trend we can see that the only other time in history stocks were this overbought was at the height of the internet bubble. This measure is not quite as highly correlated to future returns as the other two but at 74% it not that bad, either. It also looks at the largest data sample of any of them so I believe it’s worth including. At its current reading it suggests stocks should return just 0.74% per year over the coming decade.

Blending the three forecasts together we get a 0.89% annual return forecast for the stock market over the coming decade. A straight comparison to 10-year treasuries at 2.2% shows them to be the more attractive of the two asset classes right now. Hell, even 5-year treasuries are paying 1.6%, nearly double our model’s forecast.* All in all, this looks to be the second worst time to own equities in history.

Blending the three forecasts together we get a 0.89% annual return forecast for the stock market over the coming decade. A straight comparison to 10-year treasuries at 2.2% shows them to be the more attractive of the two asset classes right now. Hell, even 5-year treasuries are paying 1.6%, nearly double our model’s forecast.* All in all, this looks to be the second worst time to own equities in history.

Still, the stock market’s uptrend remains in tact as all of the major indexes currently trade above their 200-day moving averages. But as I’ve noted recently there are plenty of signs that the trend is not as healthy as bulls would hope. The advance/decline line, new highs-new lows and the percentage of stocks trading above their 200-day moving averages are all diverging fairly dramatically from the new highs recently set in the indexes. This is a serious red flag.

And now that our market cap-to-GDP and household equities indicators have possibly peaked, along with high-yield spreads (inverted), margin debt and corporate profit margins, there seems to be a very good possibility that the uptrend could be tested in short order. In fact, when I go back and look at the times when all of these indicators peaked around the same time over the past 15 years or so they coincide pretty neatly with the major stock market peaks:

| Stock Market Peak | Q1-2000 | Q4-2007 | ??? |

| Market Cap-GDP Peak | Q1-2000 | Q4-2007 | Q2-2014 |

| Household Equities Peak | Q1-2000 | Q2-2007 | Q2-2014 |

| Margin Debt Peak | Q1-2000 | Q3-2007 | Q2-2014 |

| High Yield Spreads Peak (Inv) | Q3-1997 | Q2-2007 | Q2-2014 |

| Corporate Profit Margins Peak | Q3-1997 | Q4-2006 | Q3-2013 |

So the uptrend may still be in tact but I think we have a plethora (yes, a plethora) of evidence that suggests its days may be numbered. Foreign equities have mostly given up their uptrends over the past few months and commodities, led by the oil crash, look even uglier. How much longer can the US stock market swim against the tide?

* Note: I’ve received many questions over the past few months since I first posted, “Seeing The Forest For The Trees,” about just how to go about doing this and here’s my recommendation if you don’t want to own stocks right now: Hold cash. It’s not sexy but it’s dry powder.

Now if you want to earn something rather than nothing on your cash and you’re worried about interest rates rising (and it seems everyone is) you can easily build a ladder of individual bonds rather than just buying a bond fund. The difference between owning a fund and owning bonds individually is when you own bonds directly you can decide exactly what maturities you are comfortable owning and you can always hold them to maturity if interest rates move against you. A bond fund, on the other hand, doesn’t give you that sort of flexibility.

Here’s how I would consider setting up a bond ladder right now if your goal is wait for a better buying opportunity in the stock market. Simply divide your investable funds into five equal buckets. Then invest each bucket into 1, 2, 3, 4 and 5-year treasuries, for example (you may want to choose shorter or longer durations based on your own goals). So if you have $50,000 in our example you would just buy $10k of each maturity. If the 1-year bonds mature before you find a better place to put the money then reinvest the proceeds into 5-year bonds again (as your original 5-year bonds will now be 4-year bonds and so forth). This way your blended yield on the bonds should come pretty close to the 0.89% our model suggests stocks should return without any of the heightened risk in owning equities right now.