Recently there have been numerous major economic agencies warning of the growing and severe risks in the debt markets. Investors have shrugged them off as they seem to think that their bond fund is immune as are equities. They’re not.

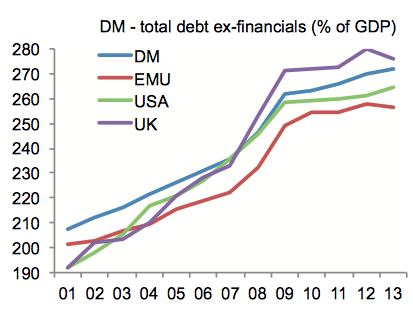

The Geneva Report, released last month, revealed that there has been no progress made in reducing debt levels around the world in the years since the financial crisis. In fact, debt levels have only grown over that time, even here in the US. This should be worrisome, they report, because, “there is considerable evidence that a high stock of debt increases vulnerability to the risk of a financial crisis.”

Chart via Geneva Report

Clearly, the BIS is looking at the same research because back in July they warned these growing debt levels could kick off ‘another Lehman.’ BIS General Manager, Jaime Caruana, told the Telegraph, “We are watching this closely. If we were concerned by excessive leverage in 2007, we cannot be more relaxed today.”

This week, the IMF joined the chorus:

…Prolonged monetary ease has encouraged the buildup of excesses in financial risk-taking. This has resulted in elevated prices across a range of financial assets, credit spreads too narrow to compensate for default risks in some segments, and, until recently, record-low volatility, suggesting that investors are complacent. What is unprecedented is that these developments have occurred across a broad range of asset classes and across many countries at the same time.

For all of these bankers, economists and regulators, there’s just too much debt for their liking and much of it carries too much risk – and it’s spread beyond the debt markets to a broad variety of other asset classes. That’s funny because even the Fed has been warning about the very same thing lately! And they’ve pointed their finger directly at the leveraged loan market.

There’s not really one definition for these things but leveraged loans are typically floating-rate loans made to companies that carry an above-average amount of debt and, for this reason are labeled, “high-yield” or “high-risk.” The “high-yield” might actually be a misnomer because lately these things have been issued at a rate of around 5%. Many of these loans are used for leveraged buy-outs and the “high-risk” label is right on the money.

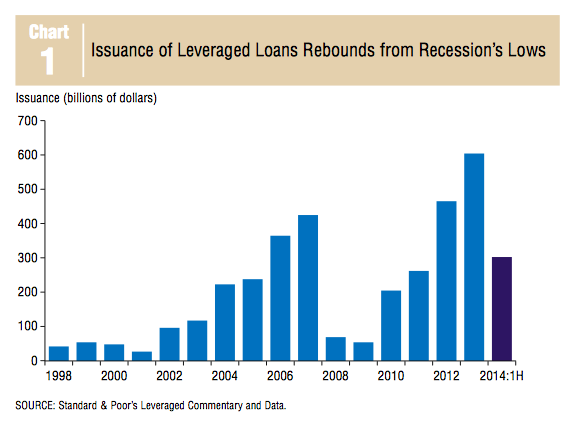

Back in 2012, the volume of these sort of loans rebounded to a new all-time record as investors, hungry for yield in a zero-interest rate environment, couldn’t get enough of them. Last year blew 2012 away and this year is on track to do even more than last.

Chart via Dallas Fed

What’s more troublesome than just the sheer volume of these loans is the quality. Although the Fed has advised bankers not to loan an amount greater than 6 times EBITDA to any given borrower, in the third quarter of this year new LBO debt levels ran 6.26 times EBITDA. This amount of leverage would normally be very risky but it is especially troublesome today because current EBITDA for these companies is based on record-high profit margins. Should margins contract at all, it would make these borrowers less likely to be able to service their debt. In other words, a simple reversion in profit margins closer to their historical average level would probably mean rising defaults, maybe dramatically so.

With yields currently at 5%, investors in these loans currently don’t need to worry about defaults hovering around the 2% level (unless you think a net 3% return is silly for the amount risk you’re taking, as I do). But prior to the financial crisis, before the s*** even began to hit the fan, default rates were nearly twice that level. At the height of the crisis defaults soared to nearly 13%. Now consider that these companies are more highly leveraged than ever and a huge portion of their debt floats at rates that are now near record lows.

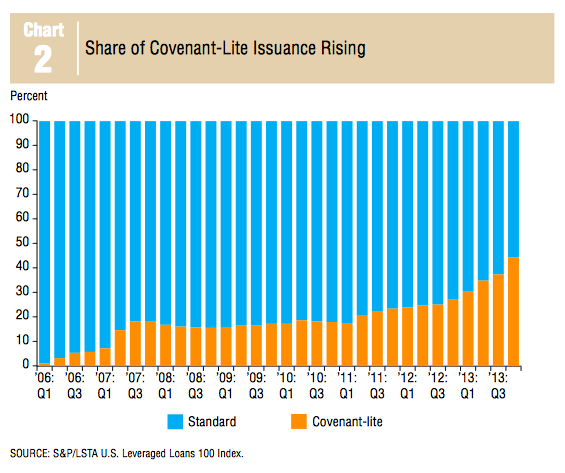

On top of that, the share of “covenant-lite” loans has soared. These are loans that place fewer restrictions on the borrowers and give lenders less recourse in the event of a default. So when (not if) defaults rise again lenders will feel more pain in these sorts of loans than they ever have before.

Chart via Dallas Fed

Richard Fisher summed it up fairly well recently saying, “the big banks are lending money on terms and at prices that any banker with a memory cell knows from experience usually end in tears.” And this time it will be more than just bankers’ tears. Shadow bankers will be affected, too. And by “shadow banking,” I mean your bond fund (among other things).

From the IMF:

While banks grapple with these challenges, capital markets are now providing more significant sources of financing, which is a welcome development. Yet this is shifting the locus of risks to shadow banks. For example, credit-focused mutual funds have seen massive asset inflows, and have collectively become a very large owner of U.S. corporate and foreign bonds. The problem is that these fund inflows have created an illusion of liquidity in fixed income markets. The liquidity promised to investors in good times is likely to exceed the available liquidity provided by markets in times of stress, especially as banks have less capacity to make markets.

This may be why the Fed has been chastising the banks so much lately. Maybe they know how much more difficult a “shadow banking” crisis would be to deal with than just your run-of-the-mill “banking crisis.”

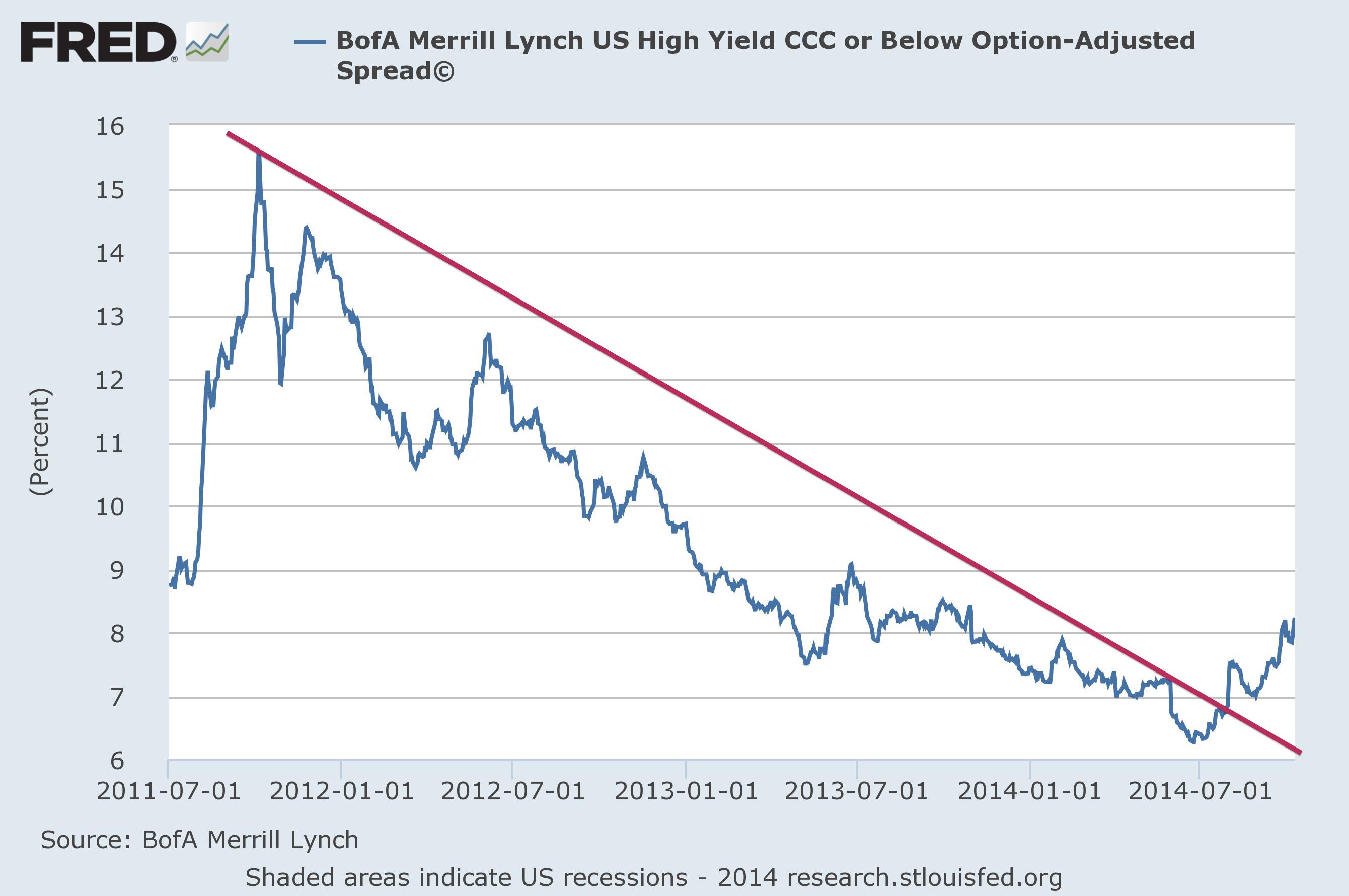

Anyhow, what is troublesome right now is that it looks like profit margins might have already begun to revert. This puts pressure on all of these highly leveraged companies and makes the prospect of defaults more likely. This is probably why credit spreads have recently widened to their highest levels of the year, breaking the multi-year downtrend that inspired the boom in the first place. All in all, this could be the beginning of the end of the “reach for yield” in this cycle.

Chart via St. Louis Fed

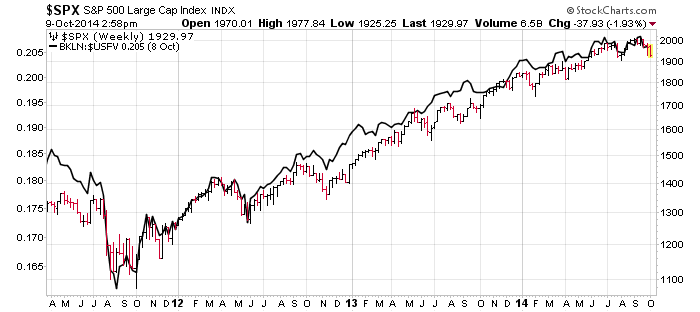

What I find most fascinating about the whole thing, however, is that the demand or appetite for leveraged loans is so closely correlated to the stock market. The black line in the chart below tracks the PowerShares Senior Loan Portfolio, a leveraged loan ETF with $6.5 billion in assets, relative to the 5-Year Treasury Note price (roughly the average weighted duration in the ETF portfolio). The S&P 500 Index is also overlaid. Clearly, the risk appetite for leveraged loans is nearly perfectly mirrored by the stock market.

Chart via StockCharts.com

Now I don’t know if this correlation will hold up going forward but it sure looks like risk appetites across asset classes are currently dancing to the same beat. And if this credit cycle is going to end in tears then it may be hard for equity investors to avoid a similar fate.